THE RE-MORTGAGE REVOLUTION. FAREWELL TO THE SURROGACY.

.

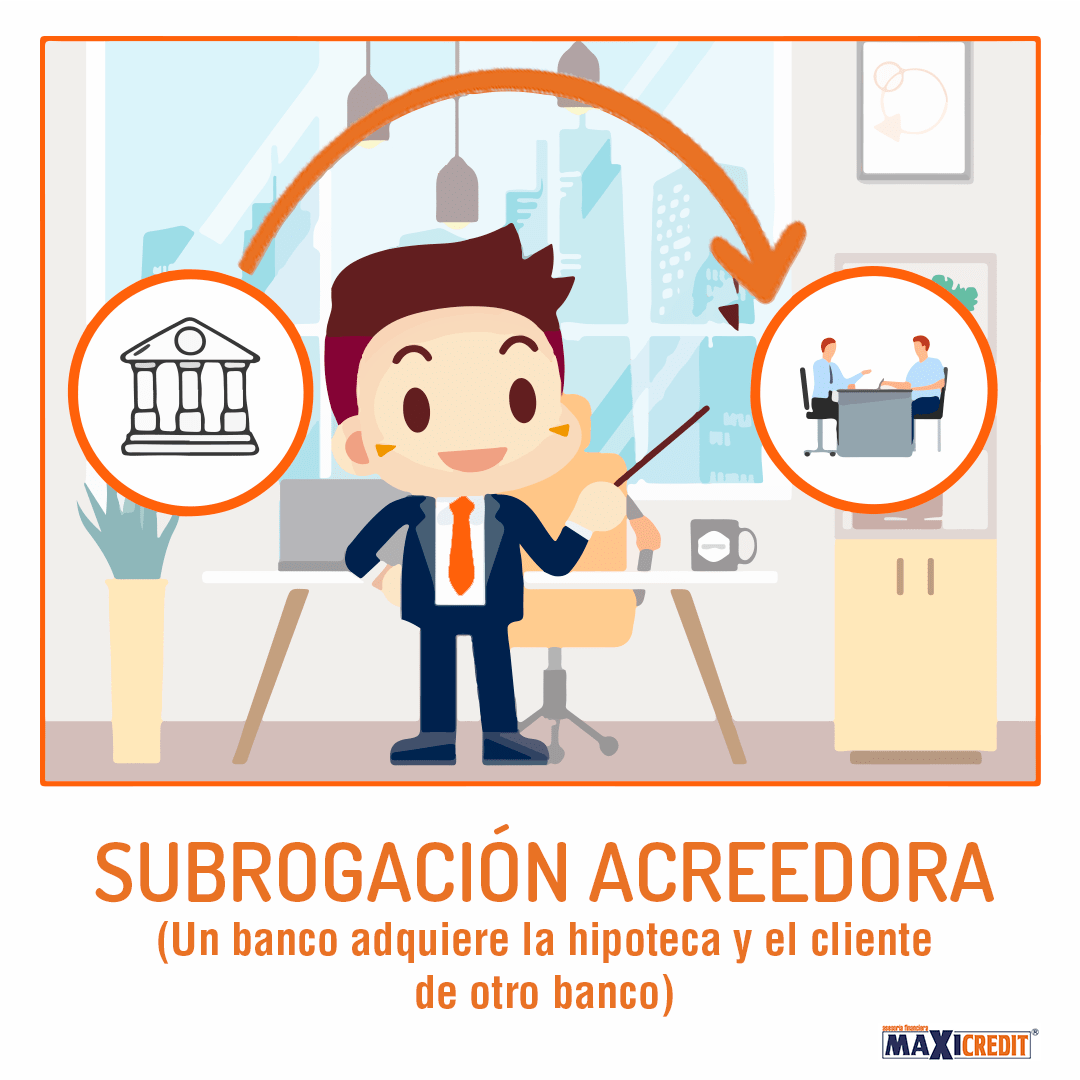

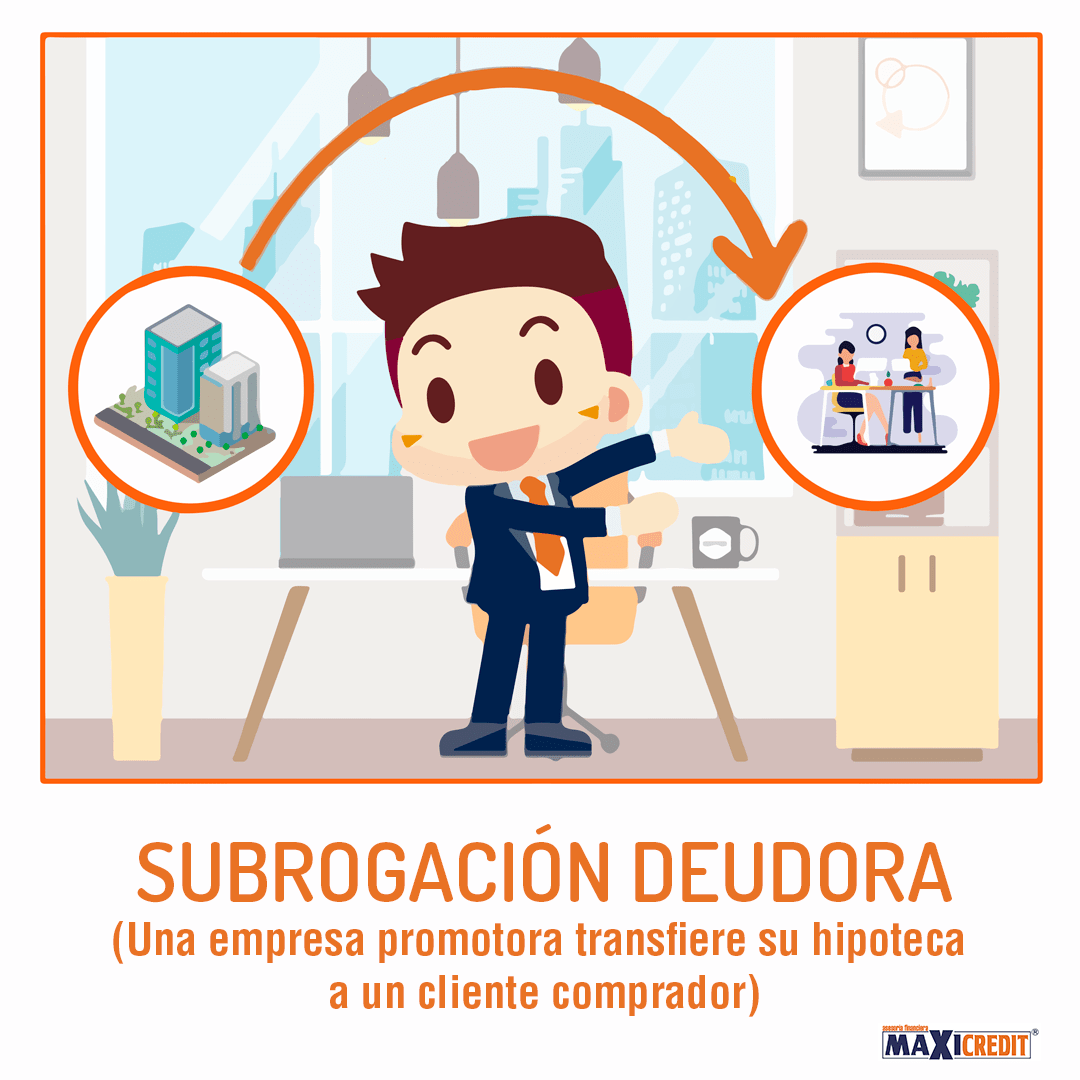

Let's briefly comment on some concepts. According to the Royal Academy of Language, surrogate is "replace or put someone or something in place of another person or thing”. In the financial sphere, we find ourselves on the one hand with the Debtor surrogacy (the customer takes the place of the bank) when for example, a client buys a newly built home and gets the mortgage that the developer had. On the other hand there is the CREDITOR OR banking SUBROGATION, which is the act by which, a bank is put in the position of another bank that already has the mortgage registered in the property register. We can say that the Bank 2 "takes the customer away" from the Bank 1 who constituted the mortgage. It is regulated by law 2/1994 de 30 and its intention was to reduce costs for consumers when switching banks and promote free competition between.

.

✔ El Cost of a surrogacy creditor to the customer: payment of the surrogacy fee (equivalent to the cancellation fee for your mortgage). For mortgages covered by the Real Estate Credits Act and after the third year of life, the commission applicable by moving from variable to fixed, must be ZERO.

"img class"emoji" draggable"false" alt"✔" src""https://s.w.org/images/core/emoji/72x72/2714.png"> The Cost of Creditor Surrogacy for the Bank 2: Notary expenses, registration and management for mortgages signed before the entry into force of the Real Estate Credits Act in 2019. And for Mortgages signed since July 2019, the bank 2, return to the bank 1, a proportional share of AJD's tax and the deed expenses it paid when the mortgage was made up depending on the remaining repayment time left on the mortgage.

.

.

.

Another action banks can take, is the Novation; which is a modification of the contractual conditions as well we can see in this link, https://www.conceptosjuridicos.com/novacion/ y it's about changing the deadline, interest rate, remove or add a headline, etc. These modifications are made by the lender under its own criteria. Let's say it's a lender's right that you can carry out or not, according to your desire or interest in the operation/client. It is also regulated by law 2/1994.

Novation cost

El cost of a customer novation, comes picked up on the mortgage deed (between the 0% and the 1% outstanding capital), but it can be agreed privately at no cost.

.

.

.

RE-HIPOTECA or mortgage re-financing. It is the act of forming a mortgage to cancel another existing. It can be carried out by the same bank that has the mortgage right, or for a different one. The Re-mortgage is going to be regulated by the mortgage law that is of 8 February 1946 with its subsequent modifications, or the new Real Estate Credit Contracts Act (Law 5/2019). The fact that it is regulated by one law or another, will depend on whether it is residential property and/or borrowers are natural or legal persons.

Rehipoteca Cost

El cost to the customer of a Re-mortgage, Be: a) the expense of canceling your current mortgage - cancellation fee, if it exists, more mortgage cancellation- and b) the payment of the appraisal and opening fee if there is a (these costs do not have to be disbursed by the customer of their own savings, because the bank could give you a little more mortgage for it).

The cost to the bank: Tax payment (AJD), notary, registration and management of the mortgage deed.

Many banks opt for re-mortgage because surrogacy for the bank involves another inconvenience and is that the bank that's going to have the customer taken away, you can take advantage of your right to enervtion and therefore, match or improve the offer presented by the bank seeking surrogacy and the customer does not change.

For all this, we're going to come across cases in which banks are going to want to attract new customers (who already have a mortgage), offering re-financing or re-mortgages and NOT surrogacy. Banks need to give mortgages and in these years of negative rates and some uncertainty in the sale of homes we will live “the re-mortgage revolution” .